Navigating Mortgage Options: A First-Time Homebuyers Guide

Discover expert tips to navigate the confusing world of mortgage options as a first-time homebuyer. Don’t miss out on savings!

Image courtesy of Valentin Antonucci via Pexels

Table of Contents

Buying your first home is an exciting journey filled with big decisions, especially when it comes to mortgages. As a first-time homebuyer, navigating the world of mortgage options can feel overwhelming. There are so many terms and factors to consider, from interest rates to down payments and loan terms. In this blog post, we’ll break down the various mortgage options available to help you make an informed decision that’s right for you.

Understanding the Basics of Mortgages

Definition of a Mortgage: A mortgage is a loan that you take out to buy a home, with the home itself serving as collateral. This means that if you fail to make your mortgage payments, the lender can take possession of your home.

Fixed-rate vs. Adjustable-rate Mortgages: With a fixed-rate mortgage, your interest rate remains the same for the entire term of the loan, providing predictability in your monthly payments. On the other hand, an adjustable-rate mortgage (ARM) has an interest rate that can change periodically, potentially resulting in higher or lower monthly payments.

Terms and Amortization: The term of a mortgage refers to the length of time you have to repay it, with common options being 15-year and 30-year terms. The longer the term, the lower your monthly payments, but the more you’ll pay in interest over the life of the loan. Amortization refers to how your loan is paid off over time, typically starting with higher interest payments that gradually shift towards paying off the principal balance.

Types of Mortgage Loans

Conventional Loans: Conventional loans are not insured or guaranteed by the government, and typically require a higher credit score and larger down payment compared to other types of loans. Private mortgage insurance (PMI) may be required if your down payment is less than 20% of the home’s purchase price.

FHA Loans: FHA loans are backed by the Federal Housing Administration and are popular among first-time homebuyers due to their lower down payment requirements and more lenient credit score standards. This can make homeownership more accessible to those who may not qualify for a conventional loan.

VA Loans: VA loans are specifically available to military veterans, active-duty service members, and eligible surviving spouses. These loans offer competitive interest rates, no down payment options, and may have lower closing costs compared to other loan types.

Tips for Choosing the Right Mortgage

Assessing Your Financial Situation: Before diving into the homebuying process, take a close look at your finances. Consider your monthly budget, credit score, and debt-to-income ratio to determine how much house you can comfortably afford. Be realistic about your financial situation and don’t stretch yourself too thin.

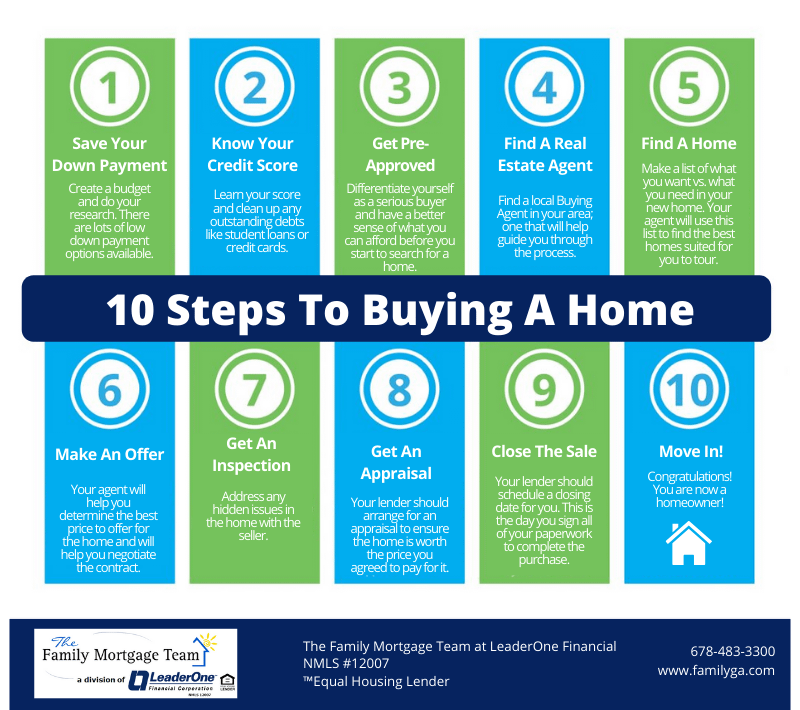

Image courtesy of familyga.com via Google Images

Shopping Around for Lenders: Don’t settle for the first mortgage offer you receive. Take the time to shop around and compare interest rates, fees, and customer reviews from different lenders. This can help you find a mortgage lender who offers competitive rates and excellent customer service.

Getting Pre-approved: Getting pre-approved for a mortgage can give you a competitive edge when making an offer on a home. Pre-approval shows sellers that you are a serious buyer and have the financial backing to make the purchase. It also gives you a clear idea of how much you can afford to spend on a home.

Pitfalls to Avoid

Taking on Too Much Debt: It can be tempting to borrow the maximum amount offered by a lender, but it’s important to consider your long-term financial health. Avoid taking on more debt than you can comfortably afford, as this can lead to financial stress and put your home at risk.

Skipping the Home Inspection: A home inspection is a crucial step in the homebuying process. An inspector can uncover hidden issues with the property that may not be immediately apparent, potentially saving you from costly repairs down the line. Don’t skip this vital step in the homebuying process.

Ignoring the Fine Print: When reviewing your mortgage contract, don’t gloss over the fine print. Make sure you understand all the terms and conditions of the loan, including any potential fees or penalties. Asking questions and seeking clarification can help you avoid surprises later on.

Buying your first home is a significant milestone, and choosing the right mortgage is a key part of the process. By understanding the basics of mortgages, exploring different loan options, and taking the time to assess your financial situation, you can set yourself up for success as a first-time homebuyer. Avoid common pitfalls, like taking on too much debt or skipping important steps like a home inspection. With the right knowledge and preparation, you’ll be well on your way to purchasing your dream home.